This is Daily Stock, delivering the core macroeconomic trends and key indicators of global financial markets.

Summary

Germany's Federation of German Industries (BDI) and the German Institute for Economic Research (DIW) have significantly lowered Germany's economic growth forecast for 2026, citing geopolitical risks.

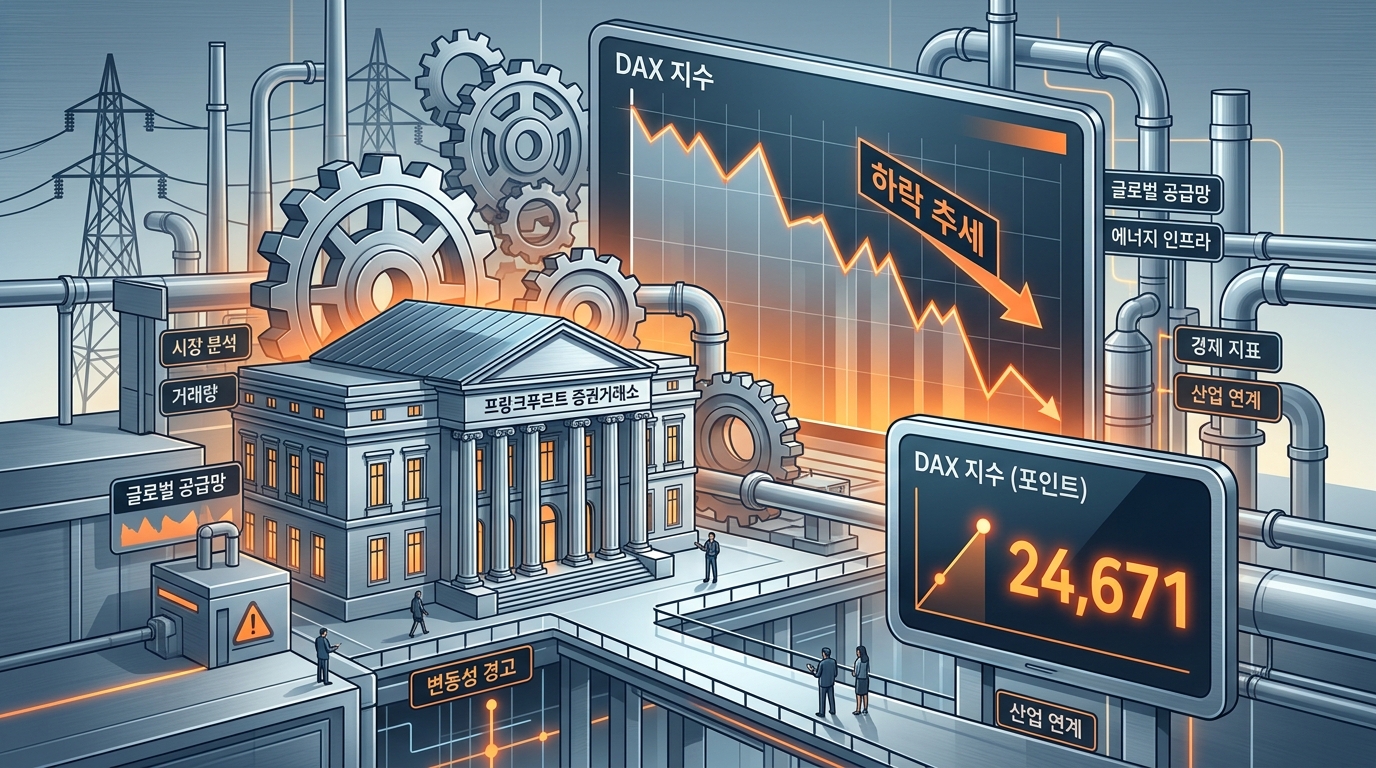

Consequently, the DAX 40 index on the Frankfurt Stock Exchange recently experienced a correction, sliding to the 24,671.22 level.

[Image: /stdaily/uploads/202606/gen_6a401e634fd2f8.76765915.png]

Germany's industrial production in April rebounded slightly by 0.4% month-on-month, avoiding the worst-case scenario.

However, long-term recession concerns are deepening due to a combination of a structural slowdown in Eurozone manufacturing and large-scale corporate restructurings.

Fundamental decoupling among the US, Asia, and Europe is accelerating daily.

Investors must closely monitor whether the slowdown in Eurozone growth will act as a downside risk for global stock markets overall.

Current Status

According to Germany's Federal Statistical Office, German industrial production in April 2026 increased by 0.4% month-on-month on a seasonally adjusted basis.

This marks a rebound after four months of decline, but opinions remain divided on the sustainability of this recovery amid ongoing Middle East tensions.

Germany's manufacturing sentiment, measured by the S&P Global Manufacturing PMI, fell to 49.9 in May.

With this figure dropping below the baseline of 50, it is evaluated as having re-entered contraction territory after just one month.

Influenced by these factors, the German DAX index closed the week at 24,671.22 points as of June 26, 2026, down 1.26% from the previous week.

As domestic and international macroeconomic uncertainties mount, short-term downward pressure on the index is gradually strengthening.

Financial Analysis

The fundamentals of large German manufacturing enterprises leading the Eurozone have taken a direct hit from the Middle East energy shock.

High energy costs and supply chain disruptions are combining to significantly increase operating expense burdens.

Germany's flagship automaker Volkswagen (VW) announced plans to cut 35,000 jobs, embarking on a massive restructuring program.

This desperate measure to overcome high cost structures and survive appears to be spreading across major German corporations.

Operating margins in traditional manufacturing sectors continue to deteriorate due to high tax burdens and rising labor costs driven by an aging population.

Conversely, some technology-focused, small-and-medium-sized machine tool exporters are showing a recovery trend contrasting with large corporations, backed by solid demand from Asia.

| Key Indicator | Latest Release (Confirmed June 2026) | Previous Value & Trend | Economic Impact |

|---|---|---|---|

| **German Industrial Production (MoM)** | 0.4% Increase (Apr) | -0.1% (Mar) | First rebound since the outbreak of the war in the Middle East |

| **Manufacturing PMI** | 49.9 (May) | 51.4 (Apr) | Re-entry into contraction & concern over capacity utilization slowdown |

| **BDI Economic Growth Forecast** | Downgraded by 0.4%p | 1.0% (Previous Forecast) | High costs & prolonged structural risks |

| **DAX 40 Close** | 24,671.22 (As of 6/26) | 25,420.66 (All-Time High) | Correction of about 3% from the peak |

Valuation

The forward price-to-earnings (Forward P/E) ratio of the German DAX index is exceptionally cheap compared to other major developed stock markets.

This stands in stark contrast to the US Nasdaq index, dominated by high-growth Big Tech, which commands a robust premium.

Compared to major Asian indices showing relative strength on the back of booming semiconductor exports, the momentum for a valuation re-rating in Germany remains very weak.

However, this reflects an economic structure centered on traditional smokestack industries and a lack of long-term growth potential, meaning it is risky to invest solely based on cheap valuation appeal.

[Image: /stdaily/uploads/202606/gen_6a401e6e9f13c3.49342250.png]

Expert & Institutional Analysis

Peter Reibinger, President of the Federation of German Industries (BDI), remarked, "German industry is currently in a very precarious position, but it is not at a completely hopeless stage."

However, he diagnosed that overcoming the recession will require cutting excessive bureaucracy and regulations, alongside bold tax benefits such as corporate tax cuts.

A McKinsey report strongly warned about the chronic productivity limits of German manufacturing.

According to the analysis, a small number of large corporations in Germany monopolize most of the productivity gains, leaving the innovation pace of small and medium-sized manufacturers sluggish.

Major financial institutions, including ING Group, also emphasize that normalizing energy supply and demand in the Eurozone must come first.

Germany's transition speed to renewable energy and supply chain diversification will be the key to restoring long-term confidence in Eurozone stock markets.

Risk Factors

The most critical threat is the geopolitical conflict in the Middle East, represented by the war involving Iran, and the resulting spike in energy prices.

Since Germany has a high share of energy-intensive manufacturing, it is highly sensitive to fluctuations in gas and electricity costs.

Weak Eurozone fundamentals, leading to a depreciation of the Euro and potential capital outflows, are also destabilizing factors for the stock market.

Amid the US Federal Reserve's high-for-longer interest rate stance, the liquidity gap continues to put pressure on Eurozone financial markets.

Investment Perspective

According to the Fear and Greed Index compiled by Daily Stock, Nasdaq is currently in the "Fear" (24.8) stage.

KOSPI is also indicating "Fear" (39), showing a strengthening risk-off sentiment globally.

In this contraction phase, whether the German DAX index falls below its strong psychological support level of 24,000 will be a key point in future technical analysis.

It is reasonable to avoid aggressive buying until clear signals of a short-term bottom are confirmed.

Investors need a patient strategy, waiting for fundamental improvements in manufacturing and the easing of geopolitical supply chain risks.

For the time being, maintaining a conservative stance while reviewing partial entry scenarios near support levels seems appropriate.

Investor Checkpoint Q&A

Q1. Why did major institutions lower growth forecasts despite the temporary rebound in industrial production?

A1. Apart from the rebound in April, prolonged Middle East tensions have caused permanent damage through persistent rises in energy costs and supply chain constraints.

Q2. What is the primary reason for the recent weakness in the German DAX index?

A2. Concerns over worsening manufacturing crises, such as Volkswagen's massive job cuts, combined with fears of soaring natural gas prices to trigger foreign selling.

Q3. How is the valuation of Eurozone stocks compared to the US or Asian countries?

A3. While relative valuation appeal is very high, they lack clear momentum such as high-growth themes or semiconductors, pushing them down the priority list for capital inflows.

Q4. Do massive layoffs by German companies act as a mid-to-long-term positive for the stock market?

A4. In the short term, they raise risks of consumption slowing down due to rising unemployment; however, in the mid-to-long term, they could help defend profit margins by restructuring high-cost operations.

Q5. What is the most critical macroeconomic indicator to monitor when investing in the DAX?

A5. Whether Germany's Manufacturing PMI recovers above the 50 mark, representing the Eurozone's overall economic contraction status, and the normalization of energy supply chains from the Middle East.